.png)

Article

The realities of Bank Statement Processing in 2025

Every day, financial services teams handle mountains of documents, and bank statements are often among the most painful.

Traditional methods employed by mortgage lenders for conducting affordability insights have proven to be expensive, time-consuming, and plagued by complex challenges, not least those relating unconscious bias and human error.

Traditional methods employed by mortgage lenders for conducting affordability insights have proven to be expensive, time-consuming, and plagued by complex challenges, not least those relating unconscious bias and human error. However, technological advancements have the potential to streamline and enhance the efficiency of these processes by up to 75%.

Affordability is an increasingly important criteria for mortgage lenders, particularly since the dramatic change in the macro-economic environment in late 2022. Although lenders had generally been content to rely on ONS data to model affordability, there is a sense that this is no longer fit for purpose, and more precise affordability assessments should be used.

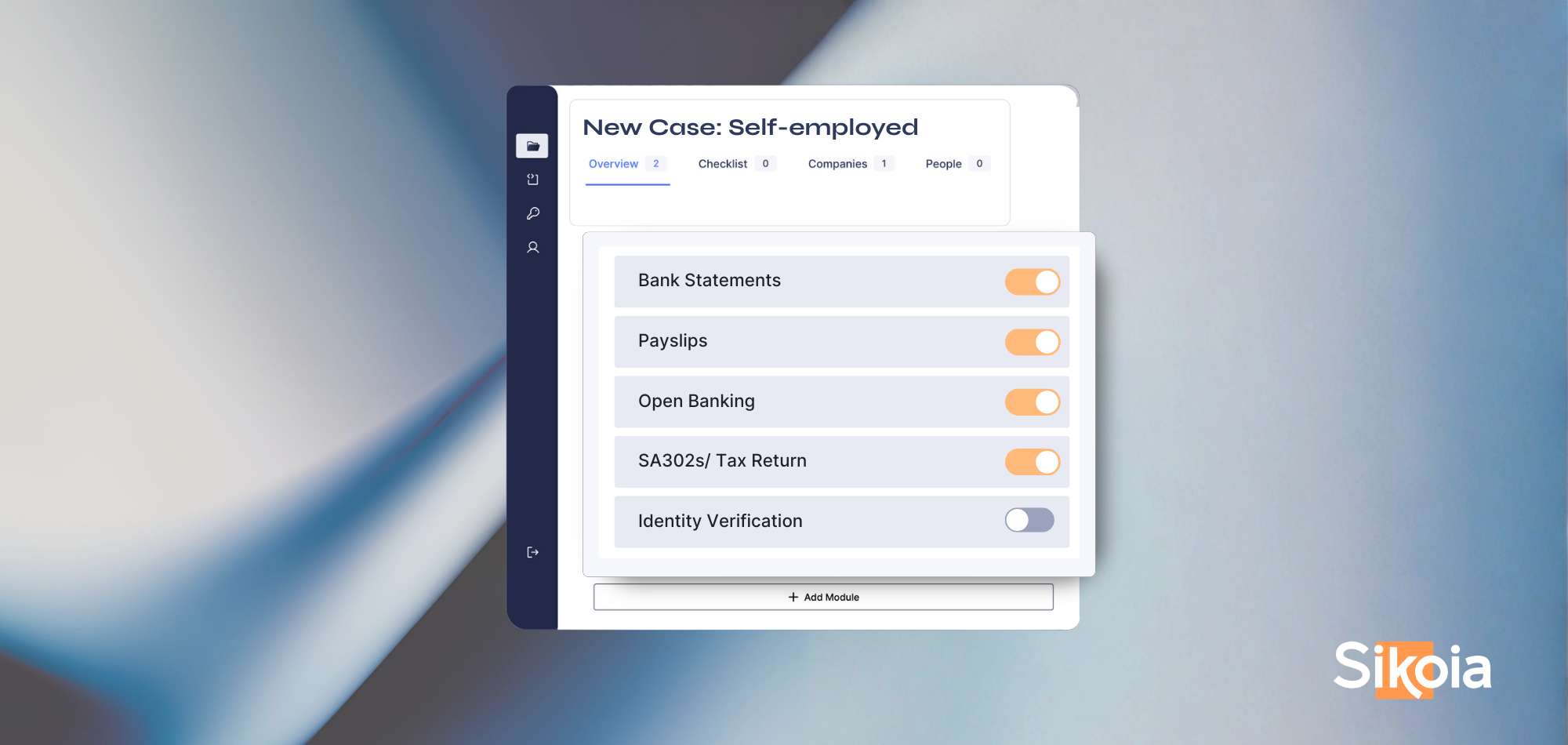

Automated Affordability Insights are the natural response. These insights involve the analysis of a customer's income and expenditures, drawn from bank statements, payslips, and credit history, to construct a comprehensive financial profile. This information is crucial for determining lending amounts and associated risk. The advantage of such an approach is that lenders can generate a bespoke understanding of each customers’ financial situation; however, this complex work depends heavily on manual underwriting teams and is extremely hard to scale.

Despite efforts to move towards technological solutions, consumers consistently exhibit a high level of distrust and low level of knowledge around the available advancements. Open Banking, which simplifies the sharing of financial information, continues to face very low consumer uptake, due to unaddressed concerns around safety and privacy. Only 16% of UK consumers surveyed in 2023 believe Open Banking is safe, and more than half of them do not understand what it is.

Manual affordability insight processes are still prevalent in today’s mortgage market, but present complex challenges.

Risk of Human Error

Human error remains a significant concern in manual data analysis. Inaccurate or incomplete readings of bank statements or other financial documents can lead to erroneous lending decisions, resulting in inconsistencies within underwriting teams and varied outcomes for customers. Spot checks, while helpful, cannot catch every error, and the lack of industry-wide consistency poses challenges.

Data Analysis is Subject to Human Biases

Differences in how individual underwriters use customer data contribute to inconsistencies across the market, raising questions about accuracy. The risk of inconsistency within a lender’s underwriting team further underscores the need for improved data analysis processes.

Manual Processes are Time-Consuming

Manual affordability assessments contribute to lengthy processing times for lenders, ranging from two days to several weeks in the most complex cases. The absence of a holistic view of a customer's finances adds further delays. The misconception that Open Banking simplifies mortgage insights persists, with only two lenders accepting open banking data as of January 2024.

Poor Customer Experience

Extended application processes can lead to customer frustration and dissatisfaction. HubSpot's 2022 marketing report reiterated that customer experience is a major factor in customer churn – a person may abandon their application midway through, or not apply for another product if they feel dissatisfied with a lender.

Even when offered Open Banking, many customers opt to manually upload their data. They may fear data breaches and privacy violations. Customers may not be aware of the strict procedures that lenders must follow to secure and store data, causing them to have a poor experience with their lender, even if the lender otherwise fulfils their expectations.

Sikoia has developed an innovative solution to address these challenges by automating aspects of data extraction and analysis, eliminating human biases and errors, improving the customer experience, and saving both time and money.

Eliminate Human Error

Sikoia’s Affordability Insights improves the spot check procedure by automating data extraction and analysis, boasting a success rate of 98 percent compared to manual extraction. This ensures a more reliable and consistent approach.

Save Time

Automatic data extraction proves to be quicker and more efficient than manual processes, making underwriters up to 75 percent more efficient. This reduction in processing time not only accelerates decision-making but also results in substantial cost savings for lenders.

Improve Customer Experience

Enhancing consistency and security, Sikoia's Affordability Insights minimises the risk of data breaches. All customers provide the same data, and underwriters access only the information they need, building trust and increasing the likelihood of repeat business.

Explore how much time and money Sikoia’s Affordability Insights can save you by using our quick efficiency savings calculator.

Sikoia Ltd is authorized and regulated by the Financial Conduct Authority (FCA) as an Account Information Service Provider (AISP) under the Payment Services Regulations 2017 (FRN: 942979) and as a credit reference provider (FRN: 942616). Sikoia Ltd is a credit broker and not a lender. Credit is subject to status.

.png)

.png)

.png)

%20(2).svg)