Compliance as a competitive edge in a changing regulatory environment

As the Fintech ecosystem and regulatory oversight evolve, we explore the emerging opportunity to leverage technology and innovation to turn compliance into a competitive edge.

By Alexis Rog • 5 min read

Fintech is entering another period of regulatory scrutiny …

Fintechs and financial innovators are no strangers to regulatory scrutiny. However, this year stands out due to heightened regulator interest in two areas: (1) the evolution of business models such as Banking as a Service (BaaS) and especially the relationship between licensed and non-licensed entities and (2) and the persistent use of regulatory arbitrage involving licenses, partnerships, and engagement with regulators across jurisdictions.

This resulting regulatory actions have significantly impacted key players globally:

Adding complexity, Fintechs must also adapt to evolving regulations, such as -for example- the full enforcement of Customer Duty in the UK in 2023 and the impending implementation of Payment Services Directive Directives (PSD3), set to take effect in the coming years.

… reshaping dynamics in an increasingly interconnected ecosystem

These specific examples are significant for the entire Fintech ecosystem because the landscape isn't just growing; it's becoming more interconnected. Many fintech successes have been built by leveraging not only others' software foundations but also their regulatory licenses. The reliance on partners' infrastructure is substantial, with over 80% of European Fintechs estimated to depend on it. Consider Revolut, for instance—part of its payment foundation rests on Modulr's infrastructure, which contributed to its ability to scale. Similarly, Shopify provides accounts via Stripe, that is in turn reliant on banks like Evolve Trust or Goldman Sachs.

We've presented a simplified flow chart illustrating the interconnected nature of the ecosystem. The 'infrastructure' category includes entities such as Electronic Money Institutions (EMIs), Banking as a Service providers, third party middleware and various others. These specific players have significantly fuelled innovation in Fintech.

As infrastructure players expand, unique dynamics and interests become increasingly apparent, especially related to risk, compliance, and growth. Each player seeks distinct benefits:

Banks partnering with Fintechs gain exposure to tech in a cost-effective way, and access to new revenue streams and markets.

Fintechs prioritise rapid business launch, bypassing the need for extensive infrastructure or banking licenses.

Customers seek seamless onboarding and convenient access to tailored and contextualised financial products

The evolving dynamics extend the banking regulatory perimeter, raising questions about ultimate accountability for onboarding, risk, and compliance. The trajectory though is clear—all players, especially non-banking entities, must elevate their standards to prevent compliance failures and ensure customer safety. Key requirements will include near real-time visibility into decisions and growing transparency between parties.

Elevate compliance to a strategic competitive advantage …

In this context, numerous Fintech players we engage with at Sikoia are reevaluating their operational models, placing a greater emphasis on compliance.

Shifting perspective, there's an opportunity to leverage technology and innovation to make compliance a competitive advantage by: (1) boosting conversion at onboarding to stand-out from competitors; (2) trim down increasing costs with new Regtech solutions and (3) adopting a proactive stance with an agile backend that adapts in line with regulations. The strategic significance is clear when considering the challenges outlined below:

… by embracing technology and fostering cultural shifts

As we conclude, Sikoia is actively involved in multiple initiatives crucial to financial services:

Data-driven transparency: centralising customer information into single master data records enhances transparency across departments and establishes clarity with third parties.

Efficient automation: leveraging Large Language Model (LLM) applications, we streamline manual analyses. Notably, our exploration of AI applications improves the accuracy of PEPs and adverse media checks, as well as automates data extraction from documents.

Adaptive decisioning: implementing modular rules engines for seamless policy adjustments.

Ongoing monitoring: event-driven monitoring of key risk indicators.

Innovation during the customer lifecycle, especially in the onboarding stage, is crucial for establishing a distinctive edge. This initial interaction sets the tone for the entire relationship, providing insight into the customer's identity and business intent.

Yet, technology's utility is limited without a shift in Fintech towards a compliance culture. Compliance should not be viewed as a growth-restraining function but as one enabling sustainable growth. Compliance innovation is not optional; it guides the Fintech ecosystem towards greater resilience, efficiency, and trust.

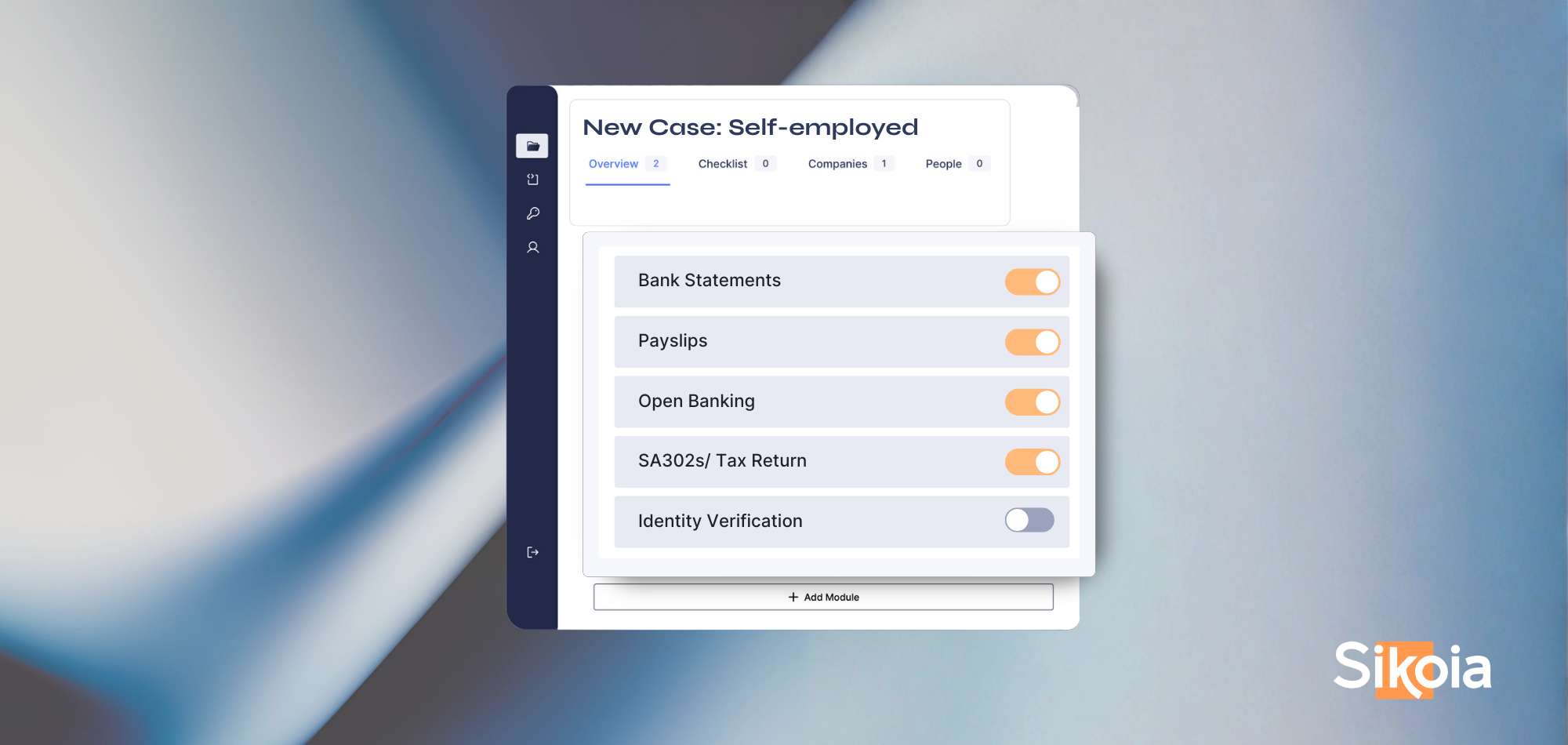

Sikoia offers a unified data platform, streamlining the compliance process and enabling fintechs to manage their compliance obligations more efficiently and effectively. Book a demo if you want to discuss how Sikoia can help you.

%20(2).svg)

.png)

.png)

.png)

.png)