.png)

Article

The realities of Bank Statement Processing in 2025

Every day, financial services teams handle mountains of documents, and bank statements are often among the most painful.

Mortgage lenders is at a crucial juncture. Embracing advancements is imperative for navigating the ever-evolving landscape and elevating their risk management capabilities.

Mortgage lenders face a significant challenge adapting their risk assessment methods to streamline processes and allow underwriting teams to concentrate on tasks that genuinely demand their attention.

Why Risk Assessments Are Important

Efficient risk management is pivotal for lenders aiming at sustained profitability and positive cash flow. Key decisions, such as loan amounts, interest rates, and repayment terms, hinge upon meticulous risk assessments. Neglecting responsible risk management may lead to customer defaults, leaving lenders without repayment.

Moreover, compliance with Financial Conduct Authority (FCA) regulations requires lenders to gauge applicants' ability to repay loans. Lenders must be able to demonstrate that they have exercised due diligence in assessing borrowers, or face stiff penalties.

Regardless of their compliance requirements, lenders currently also face concerns over the affordability of mortgage repayments as rising costs put pressure on homeowners. The swift surge in interest rates, escalating from 1.2% in September 2021 to 5.94% in September 2023, intensifies the need for effective risk management in an increasingly volatile mortgage market.

Challenges with Current Risk Assessments

The UK mortgage market is already grappling with the lowest approval rates since 2009 (excluding Covid). Simultaneously, a surge in consumer credit utilisation reveals a populace grappling with soaring expenses. Enhancing the precision of risk assessments empowers lenders to navigate economic uncertainties with confidence.

Current risk assessments often rely on time-consuming manual analyses by underwriting teams. Affordability checks, typically taking up to 48 hours, present a financial and operational strain for lenders and frustrate applicants, some of whom may abandon the process due to extended wait times. Complications arise when applicants have multiple bank accounts, or lack access to Open Banking, adding complexity to an already intricate application process.

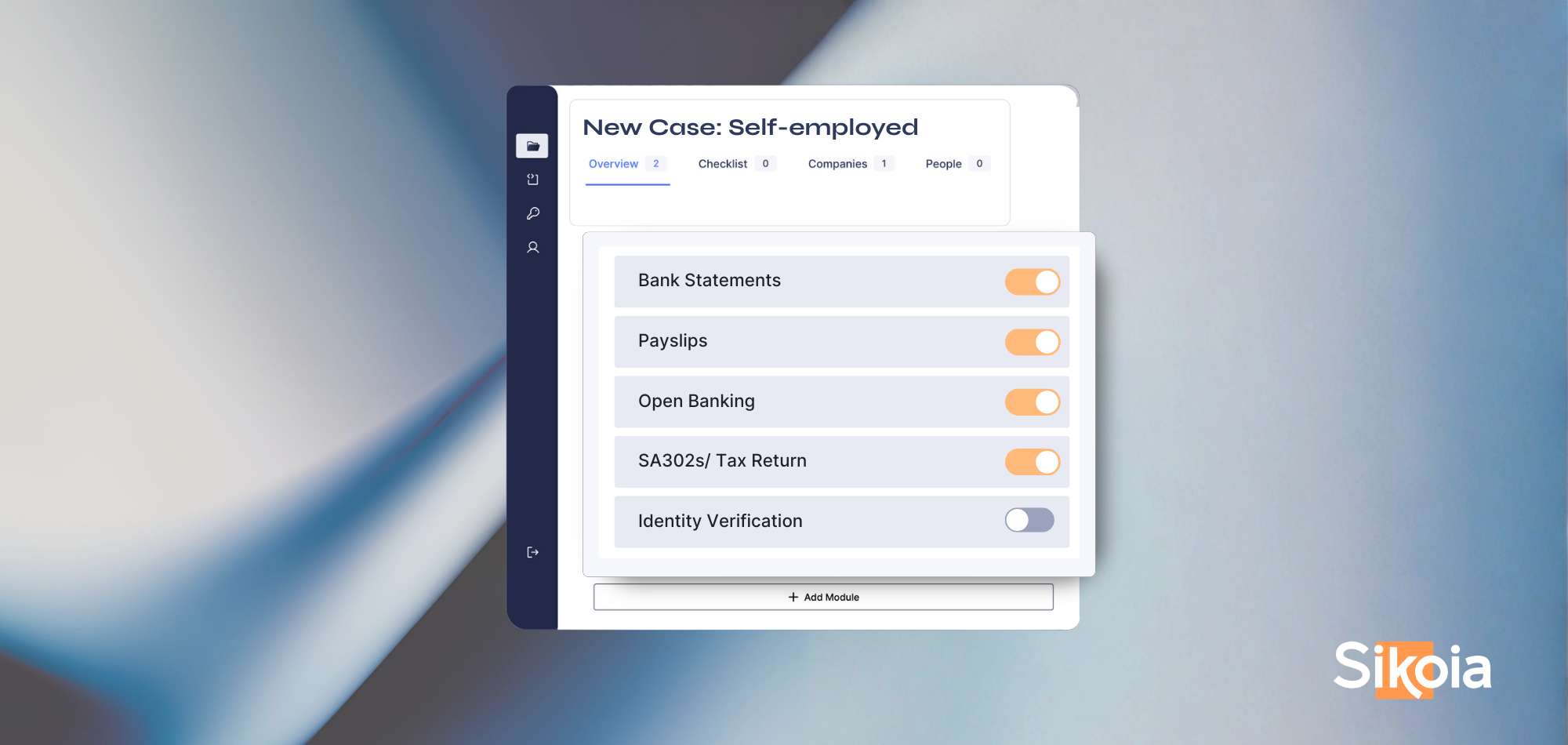

Consider the mandatory submission of three months' worth of bank statements for a mortgage application. While obtaining statements is simple for applicants, the challenge lies in lenders deciphering the information through manual and outdated processes, causing delays.

Technological Advances and Machine Learning

Continuous technological advancements offer a glimmer of hope for lenders grappling with risk assessment challenges. Sikoia’s Affordability Insights solution, powered by automation, alleviates the burden on underwriters, freeing up time for more strategic aspects of their role.

This innovative approach significantly enhances the ability to detect inconsistencies in customer data, reducing the risk of fraudulent documents such as fake bank statements or pay slips.

While the financial industry experiences rapid transformations, only time and rigorous testing will reveal the technologies that genuinely revolutionise existing processes.

Mortgage lenders, now at the crossroads of tradition and innovation, must embrace advancements to navigate an evolving landscape and enhance their risk management capabilities.

Sikoia Ltd is authorized and regulated by the Financial Conduct Authority (FCA) as an Account Information Service Provider (AISP) under the Payment Services Regulations 2017 (FRN: 942979) and as a credit reference provider (FRN: 942616). Sikoia Ltd is a credit broker and not a lender. Credit is subject to status.

.png)

.png)

.png)

%20(2).svg)