.png)

Article

The realities of Bank Statement Processing in 2025

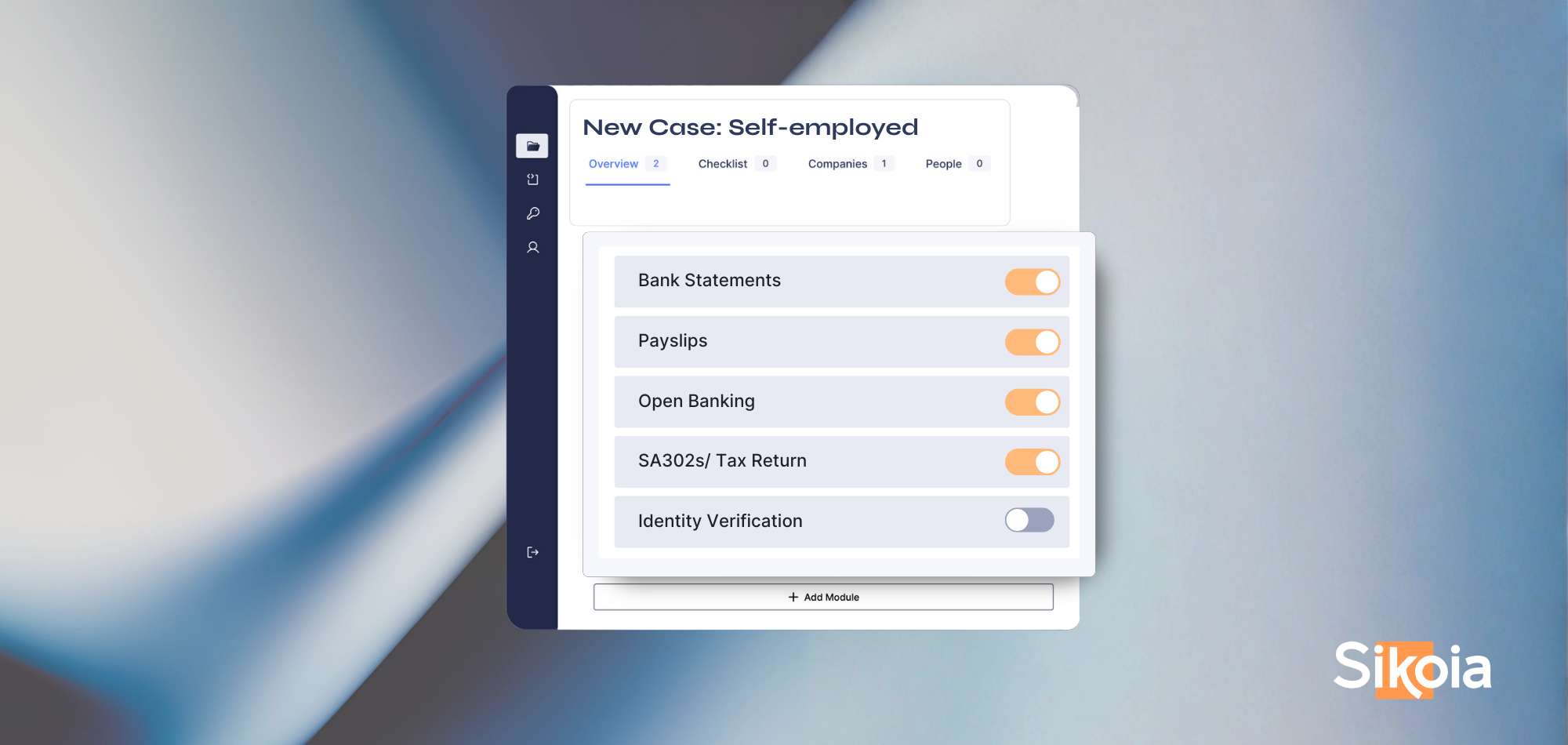

Every day, financial services teams handle mountains of documents, and bank statements are often among the most painful.

The recent UK election brought a Labour government aiming to reshape the mortgage market with ambitious housing plans and stricter regulations. This blog explores the impacts on mortgages and the essential role of customer verification and onboarding.

The recent UK election resulted in a Labour government, promising significant changes to the financial and housing markets. Labour, whose key focus as they begin their term is to tackle longstanding issues of housing supply, affordability, security, and quality. They have an ambitious target of building 1.5 million new homes within their government tenure. This shift brings with it a range of policies aimed at reshaping the landscape for mortgages and homeownership, particularly through new regulations and risk assessment practices.

Let’s explore what some of these changes mean for the mortgage market and how they tie into the challenges of customer verification and onboarding.

Labour’s commitment to increased regulation may have a direct impact on the mortgage market. Stricter oversight of financial institutions means more robust consumer protections, ensuring fairer treatment for borrowers. This includes caps on fees and interest rates, making mortgages more affordable for many. However, increased regulatory scrutiny also means that mortgage providers will need to enhance their compliance frameworks to avoid penalties and ensure smooth operations.

A cornerstone of Labour’s policy is the ambitious plan to build 1.5 million new homes over eight years. This significant boost in housing supply aims to address the chronic shortage, making homeownership more attainable and stabilising property prices. However, achieving this target within the projected timeframe remains a challenge due to historical construction rates and the complexities of large-scale development projects.

Labour plans to introduce government-backed mortgage schemes to support first-time buyers. These schemes will provide more accessible financing options, reducing the barriers to entry for young and low-income buyers.

The Freedom to Buy scheme for example aims to make homeownership more accessible by offering government-backed loans or shared ownership options. This initiative introduces new challenges for mortgage providers, particularly in customer verification, affordability assessment, and risk management:

As mortgage providers adapt to new regulations and increased demand from first-time buyers, the need for efficient and effective customer verification and onboarding processes becomes critical. Labour's policies could lead to:

Sikoia’s mission is to simplify customer verification and onboarding processes, ensuring that eligible applicants can access these benefits without unnecessary delays or complications. Sikoia’s expertise in document verification and regulatory compliance can help mortgage providers navigate any regulatory changes effectively.

Labour’s victory signals a new period for the UK mortgage market. Increased regulation, a push for affordable housing, supportive mortgage schemes, and a focus on robust customer verification and onboarding processes are set to create a more equitable environment for borrowers. However, the successful implementation of these policies will be crucial in realising their full impact.

Sikoia Ltd is authorized and regulated by the Financial Conduct Authority (FCA) as an Account Information Service Provider (AISP) under the Payment Services Regulations 2017 (FRN: 942979) and as a credit reference provider (FRN: 942616). Sikoia Ltd is a credit broker and not a lender. Credit is subject to status.

.png)

.png)

.png)

%20(2).svg)