.png)

Article

The realities of Bank Statement Processing in 2025

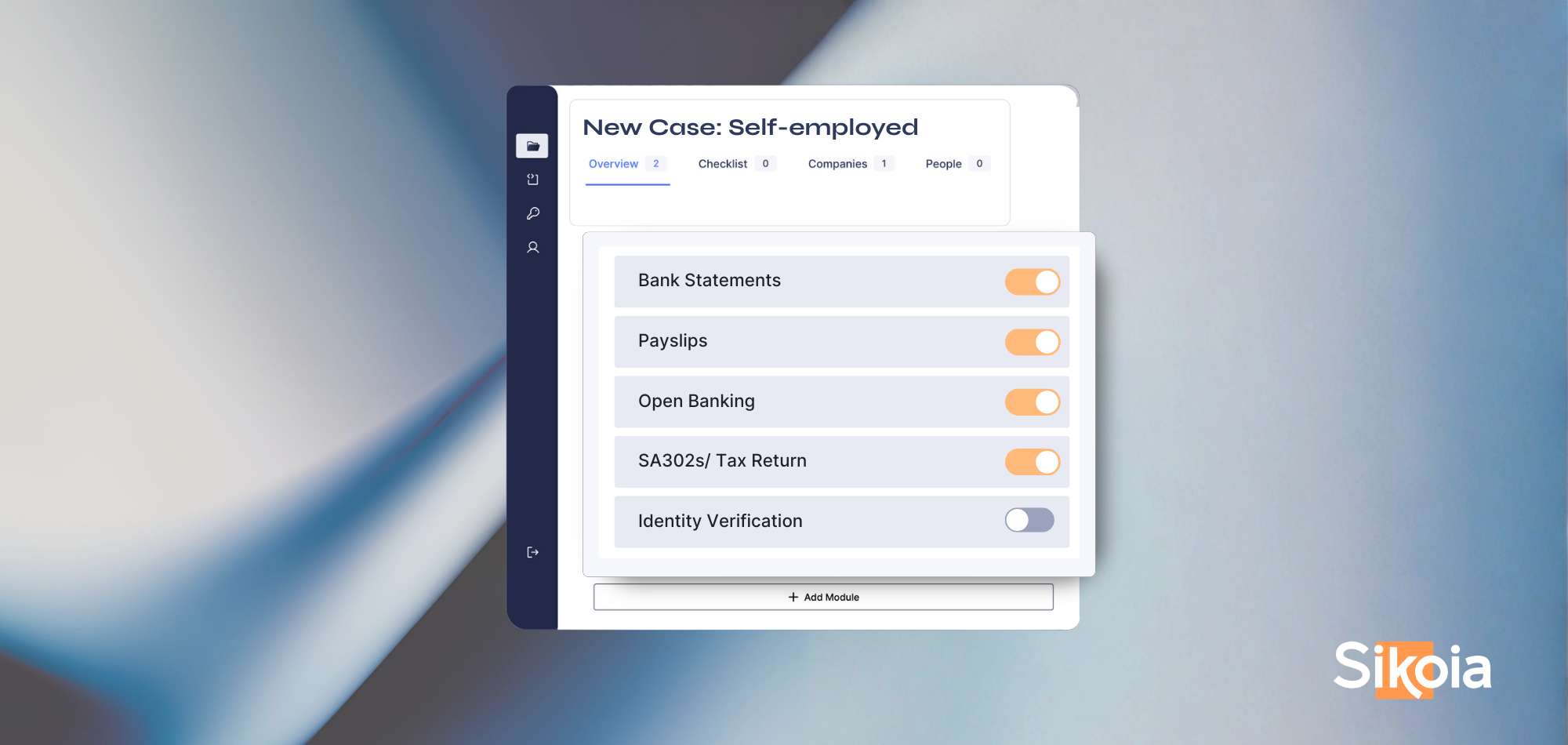

Every day, financial services teams handle mountains of documents, and bank statements are often among the most painful.

As the deadline for the Consumer Duty rapidly approaches, the Financial Conduct Authority (FCA) urges financial service providers to proactively prepare and meet the upcoming requirements.

With the deadline for the Consumer Duty rapidly approaching, the Financial Conduct Authority (FCA) has called on financial service providers to ensure they are prepared to meet the new requirements. A recent survey by Consultancy Bovill revealed that nearly half are uncertain about the time needed to implement this regulation - as is to be expected with a new suite of regulatory requirements. But a deeper look at some of the implications and consequences suggests that the providers who adapt best will thrive.

In this blog, we explore the impact of Consumer Duty on financial services, highlighting its key outcomes and outlining ways firms can adopt a customer-centric approach to drive their success.

The Consumer Duty is a new FCA obligation that applies to any firm involved in determining outcomes for retail customers, including SME customers. Its overarching goal is to promote positive customer experiences, protect consumers from financial harm, and enhance the competitiveness of the financial services sector. The Consumer Duty is defined by four key outcomes that financial service providers must adhere to:

The Consumer Duty brings a wave of regulatory changes, representing both a challenge and an opportunity for financial service providers. Some have expressed concerns over the additional administrative and operational burdens that the regulation may impose, particularly for companies already operating on tight margins. However, if implemented correctly, the Consumer Duty can prove beneficial for firms in multiple ways.

“The FCA expects companies to monitor, regularly review and assess for risks to good consumer outcomes. This requires extensive data collection, customer research and analysis.”

To effectively navigate the Consumer Duty and harness its potential benefits, financial service providers must adopt an "outside-in" approach that revolves around customer experiences and needs. This means consistently evaluating customer feedback and insights to shape products and services. Here are some key steps for success:

At Sikoia, we think one of the easiest ways financial service providers can be ready to succeed in this new environment is by deeply embedding a unified approach to data into their systems and processes. By bringing all your customer financial and identity data together in a single layer, it becomes easier to surface meaningful, customer-centric insights – and easier to embed these into all your customer touchpoints.

As the Consumer Duty deadline approaches, financial service providers must prepare to meet the new requirements to protect consumers and strengthen their business operations. While challenges exist, embracing the Consumer Duty should lead to increased customer loyalty and a competitive advantage. By adopting a customer-centric approach and adhering to the four key outcomes, firms can create positive consumer experiences, foster trust, and thrive in the evolving financial services landscape.

Sikoia Ltd is authorized and regulated by the Financial Conduct Authority (FCA) as an Account Information Service Provider (AISP) under the Payment Services Regulations 2017 (FRN: 942979) and as a credit reference provider (FRN: 942616). Sikoia Ltd is a credit broker and not a lender. Credit is subject to status.

.png)

.png)

.png)

%20(2).svg)