Affordability assessments are critical for lenders, credit providers, and financial institutions across sectors like mortgage lending, consumer credit, and auto financing. These assessments determine whether applicants can realistically afford the requested credit based on their income, expenses, and overall financial situation.

However, conducting accurate affordability checks has long been a major challenge. Each year, companies must manually review vast volumes of customer-supplied bank statements, payslips, tax returns, and other financial documents. This laborious process is riddled with inefficiencies, leading to lengthy delays, escalating operational costs, and inconsistent decision-making.

This blog post will explore what affordability checks entail, how they are traditionally conducted, the bottlenecks and inefficiencies plaguing current manual processes, and innovative ways to overcome these challenges through automation.

What are Affordability Assessments?

Affordability checks, also known as income and expenditure assessments, are a legal requirement under responsible lending regulations. They protect both the lender and the borrower by ensuring credit is only provided to those who can realistically make the required payments without falling into problematic debt.

Lenders must collect detailed information about the applicant's income sources, core living costs, existing debt obligations, and discretionary spending habits. This data is then thoroughly analyzed to calculate disposable income and determine maximum affordable repayment amounts.

How is Affordability Assessed?

Lenders use various methods to evaluate and verify an applicant's stated income, expenses, and creditworthiness during the affordability assessment process:

- Income Documentation: Lenders require evidence like payslips, tax returns, bank statements, and employment details to validate earned income amounts.

- Credit Reports: A credit check provides insights into existing debt levels, repayment histories, and overall credit risk profiles.

- Expenditure Analysis: Categorising spending patterns from bank statements and estimating reasonable living costs based on household composition.

- Income Multiples: Lenders calculate loan to income ratios and limit most mortgages to 4-5 times the applicant's annual income, for both risk considerations and PRA rules that cap larger lenders to 15% of mortgages above a 4.5 LTI ratio. (source)

- Affordability Calculators: Sophisticated algorithm-based calculators analyse all data points to recommend maximum borrowing limits.

Current Challenges with Affordability Assessments

Affordability assessments are a crucial aspect of the lending process, especially for mortgage providers in the financial industry. However, current practices face significant challenges that hinder efficiency, consistency, and profitability. These assessments heavily rely on data extracted from various documents, necessitating substantial manual effort from underwriters and processing teams.

The manual handling of application documents, such as income statements, bank statements, and credit reports, is labor-intensive and time-consuming. This not only leads to operational inefficiencies but also introduces inconsistencies due to human error and varying interpretations across different underwriters. These delays and errors can significantly undermine the customer experience, leading to frustration, decreased trust, and potential loss of business for the lender.

For mid-sized financial institutions writing between £5 billion and £6.5 billion in new gross mortgage lending annually, the operational costs associated with manual document handling and affordability assessments range from £750,000 to £1 million. However, the true financial impact extends far beyond these direct costs. When factoring in the costs of lost applications due to processing delays and the expenses of reviewing and correcting manual errors, the total costs can escalate to £1.7 million to £2.2 million for institutions of the same size.

Limitations of Current Solutions

While technologies like cloud-based Optical Character Recognition (OCR), open banking, and transaction categorization have emerged in recent years, these standalone solutions have failed to meet the crucial criteria of accuracy, cost-effectiveness, usability, and widespread adoption in the mortgage industry.

Traditional OCR software faces limitations such as high processing costs, low accuracy rates, and a lack of contextual and semantic understanding. Additionally, its per-document or per-page costs often render it uneconomical for mortgage and lending applications.

Open banking, while successful in certain areas of financial services like consumer lending, has struggled to gain traction in the mortgage industry due to factors like the highly intermediated nature of the business and consumer reluctance to share extensive banking information.

Transaction categorization players leveraging open banking prove suboptimal for income and key recurring expenditures like rent and mortgage payments. Moreover, they often fail to utilize contextual information across documents and customer data to enhance their output.

Emerging payroll and tax API solutions requiring customer consent and logins have seen even lower adoption rates than open banking and are generally not accepted by mortgage brokers. Additionally, HMRC has yet to release an API for automated tax return retrieval.

When it comes to affordability assessments, lenders often use ONS norms as simple proxies for customers’ actual expenditure. But being derived from broad statistical measures, they can fail to capture local variations in costs. And of course, they cannot track customers’ specific situations. More accurate results are possible when bank data is available to calculate customers’ actual expenditure, either using that directly or building a hybrid solution combining both sources.

The Significance of Automation

As the mortgage industry continues to evolve, lenders and credit providers must embrace automation to streamline the affordability assessment process. By leveraging advanced technologies such as document intelligence and machine learning, lenders can significantly reduce manual efforts, improve data accuracy, calculate more accurate risk scores, and provide a superior customer experience.

Automated document processing solutions can extract relevant information from customer-supplied documents, verify income sources, cross-check expenses, and feed accurate data into sophisticated affordability calculators. This not only ensures compliance with responsible lending regulations but also enables lenders to make well-informed decisions based on an applicant's true financial situation.

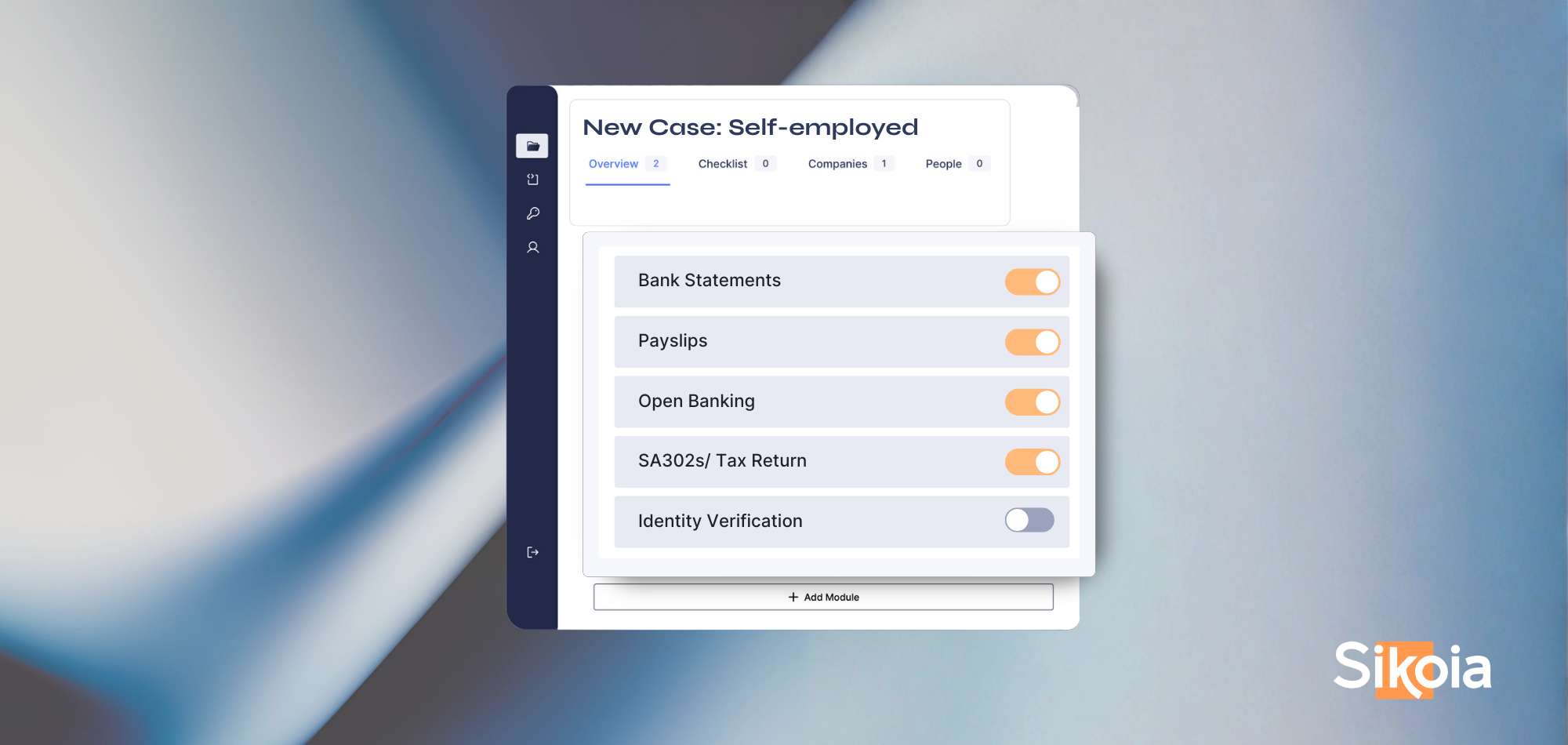

Sikoia's Unique Solution Tailored to improve the Affordability Assessments process

Sikoia is the only provider capable of accepting and triangulating customer data from bank statements, payslips, SA302s, and open banking to generate insights specifically crafted for the UK financial industry. Leveraging proprietary validation and accuracy assessments, along with sophisticated models recognizing contextual information across documents, Sikoia adeptly tackles complex scenarios such as those involving self-employed individuals and joint applicants.

The Sikoia platform revolutionises traditional processes by automating tasks previously handled manually:

- Income & Employer Verification: Eliminate manual reviews of payslips, tax returns, or bank statements by automatically generating proof of income and employer information, cross-validated and integrated back into your systems.

- Automated Affordability Insights: Generate an accurate picture of customers' affordability using verified and up-to-date data, cutting manual work by over 75% and ensuring consistency in decision-making. The categorised monthly expenditure output can be used directly, or combined with ONS-based expenditure norms. ONS norms, being statistical averages, don’t reflect the specific circumstances of each individual applicant.

- Automated Flags for Upsell and Risk: Instantly identify relevant flags, risk indicators, and inconsistencies, minimizing operational and regulatory risk.

- Validation Checks: Provide real-time feedback on the completeness of applications upon document submission.

- Data Pre-Population: Effortlessly pre-populate data in decisioning systems and front-end portals, eliminating duplicative manual data entry.

Conclusion

The traditional manual review process for these documents is a significant bottleneck, leading to substantial delays, financial costs, and a subpar customer experience. On average, it takes around 23 days to complete the end-to-end mortgage process, with a staggering 45% of that time (approximately 1-2 weeks) dedicated to obtaining and reviewing required documents from customers.

By integrating advanced technologies with industry-specific expertise, Sikoia offers a solution that addresses the complex needs of mortgage providers with unparalleled precision and effectiveness. Learn more by watching Sikoia’s video demonstration here.

.png)

.png)

.png)

.png)

%20(2).svg)